Fairly, this is a question that seems top of mind for pretty much everyone. So we thought we would equip you with some basics to help answer this question should it come up with your family, friends, neighbors, or you are taking your role as a Utah Energy United ambassador zealously and proactively – educating everyone you can!

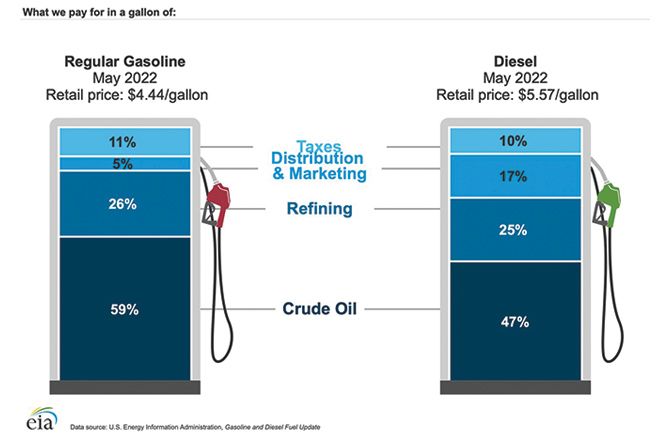

What We Pay for in a Gallon of Gas

- First and Foremost, the biggest price driver by far is the cost of crude. The cost of crude is set by the global market, primarily by supply and demand. Typically, when the cost of something goes up, the demand drops; basic Economics 101. That demand response has been slow in arriving, although we started to see demand easing at the end of July. This meant, however, that demand didn’t drop for many months to let supply catch up and we have been very tight in crude supply, which drives up the price.

- Refining is the second largest cost driver but not only are U.S. refineries working at full capacity, but the U.S. is also losing refining capacity, leading further to supply crunches. Read more below on how these challenges play into supply, demand and pricing.

- Gas Taxes are a very small percent of the total cost at the pump, so policies to provide for gas tax holidays will hurt the transportation budgets that those taxes go to fund, without significantly helping to drop prices at the pump. The Utah gas tax is approximately 32 cents/gallon, and the federal tax is 18.4 cents – the total tax is about 50 cents/gallon – mid-range compared to the rest of the nation’s rates.

Crude Oil Supply Has Tightened Dramatically

- When the global economy shut down due to COVID, demand for fuel plummeted and so both refineries and crude production responded by also turning down. But crude production isn’t easy to simply turn back on quickly – not only are we facing the same supply chain challenges (with 200-300% price increases on steel and parts) and labor shortages that the rest of the economy is seeing, but we are also operating in a highly regulated environment where there is a long runway to drill new wells to increase production.

- Politics are another factor: President Biden campaigned on no new drilling and then started to make good on that promise on his first day in office – that has resulted in a very real challenge to secure the necessary capital to drill new wells and expand production. Policy and rhetoric matter and when our leadership attacks an industry, the banks and financing entities make note of that capital risk.

- Global politics also influence prices. We are often asked how impactful is Russia and the war in Ukraine on our fuel prices? The short answer is that there is a definite influence, but the White House trying to brand the dramatic energy price increases as “Putin’s price hike” is disingenuous. It is certainly true that Putin’s invasion of Ukraine has increased global oil prices, but it doesn’t let President Biden off the hook for his anti-oil and natural gas policies. According to data from the Energy Information Administration, the price of gasoline at the pump has increased every month during the Biden Administration. On Inauguration Day in 2021, the price of WTI was $53.40 a barrel. On Feb. 24, 2022, the day Russia invaded Ukraine, the price of WTI was $99.66 – an 87% increase. The increase caused by the invasion of Ukraine occurred on top of dramatically higher oil prices over the past year and cannot all be blamed on Vladimir Putin.

Shrinking U.S. Refining Capacity Also Tightens Supply

- But even as the supply of crude starts to catch up, we then need to have refining capacity available.

- The challenge is that the U.S. has lost more than 1 million barrels a day of refining capacity. The U.S. consumes 9.2 million barrels a day of gasoline, so this is a significant loss. If projections and politics suggest there will be lower sustained demand in the future, the economic course of action may be to shutter capacity where competitiveness and profitability are in question. That has happened in the United States over the past couple of years.

- Refinery utilization rates also matter. As of July 1, U.S. refineries were operating at an average utilization rate of nearly 95%, which is very high. In normal years, U.S. refineries typically operate at around 90% of utilization or higher, as you can see:

- 2021: 86% (COVID impact)

- 2020: 79% (COVID impact)

- 2019: 91%

- 2018: 93%

- 2017: 91%

- 2016: 90%

- 2015: 91%

- 2014: 90%

- What this means is that we can’t push much more on our existing refining fleet; they are running full out, including here in Salt Lake City.

- Even with 1.1 MMBD less refining capacity, the United States is manufacturing more gasoline, diesel and jet fuel than any other country, supplying both our domestic and the global market. Our near 95% utilization rate (the highest in the world) means we’re processing about 17 million barrels of petroleum every day.

The Power of the Free Market

- Our refineries make up more than 30% of the refining capacities in the Rockies region. We need to layer in the fact that we live in a market economy where local and regional supply and demand play a role in pricing. Not only is Utah somewhat of an island, with limited crude and finished product pipelines incoming, but the regions that we supply finished product to from our refineries are even more limited in terms of options for the finished product.

- Utah has one finished product pipeline coming in:

- The Pioneer petroleum product pipeline carries refined fuel to Salt Lake City from the Sinclair refinery in Wyoming.

- Most of the fuel we use here in the state and especially along the Wasatch Front is produced from our local refineries.

- We have two product pipelines that carry refined petroleum product out of Utah:

- The Marathon line supplies markets in the Northwest (Idaho, eastern Washington, Oregon)

- The UNEV line delivers product to Cedar City and on to Las Vegas.

- Prices in Nevada, Washington and Oregon, where we supply finished product to, impact prices here in SLC. On a given day in late July, for example, the average sales prices in our export markets were impacting prices in Salt Lake:

- Average gas price Nevada: $5.558

- Average gas price Washington: $5.474

- Average gas price Oregon: $5.487

- Average gas price in SLC: $5.07

- Updated prices can be found here:

https://gasprices.aaa.com/state-gas-price-averages/

- Prices are typically cheaper in the eastern half of our country where there are more pipelines and options for barge cargos – whether that be domestic or imported product.

- There have also been accusations that oil and gas execs are keeping prices at the pump high on purpose to boost the value of their significant ownership interests in those companies. So then, who owns America’s natural gas and oil companies?

- Millions of Americans – through retirement funds like 401(k)s and private and public pension funds (typically accessible by groups including teachers and firefighters) and other investments.

- The percentage owned by individuals – corporate officers and retail owners – is just 2.4%, opposite of the repeated claim that large amounts of natural gas and oil industry stock are owned by oil and gas corporate officers.

- Similarly, who owns gas stations?

- Refiners own less than 5% of the 145,000 retail stations across the country.

- When a station bears a particular refiner’s brand, it does not mean that the refiner owns or operates the station. The vast majority of branded stations are owned and operated by independent retailers licensed to represent that brand.

- According to the National Association of Convenience Stores (NACS), more than 60% of the retail stations in the U.S. are owned by an individual or family who owns a single store where gasoline is already a loss leader to get people in the door to buy higher margin items.

- Wrapping this all together, the supply chain and ownership chain to get crude oil out of the ground and into your gas tank is long – with many independently owned stops along the way – all responding to the power of the free market.

Reading the Tea Leaves

- At the end of July we started to see some price drops. Analysts believe much of that is in response to speculation about the looming recession more than any fundamental change in supply and demand.

- It’s safe to assume that there will be a downward adjustment in demand after the summer driving and vacation season, which should also provide some relief.

- The industry is also working diligently to increase supply and hopefully we’ll see some relief there in the coming months as well.